Most Florida Retirement System employees in the Pension Plan believe one thing:

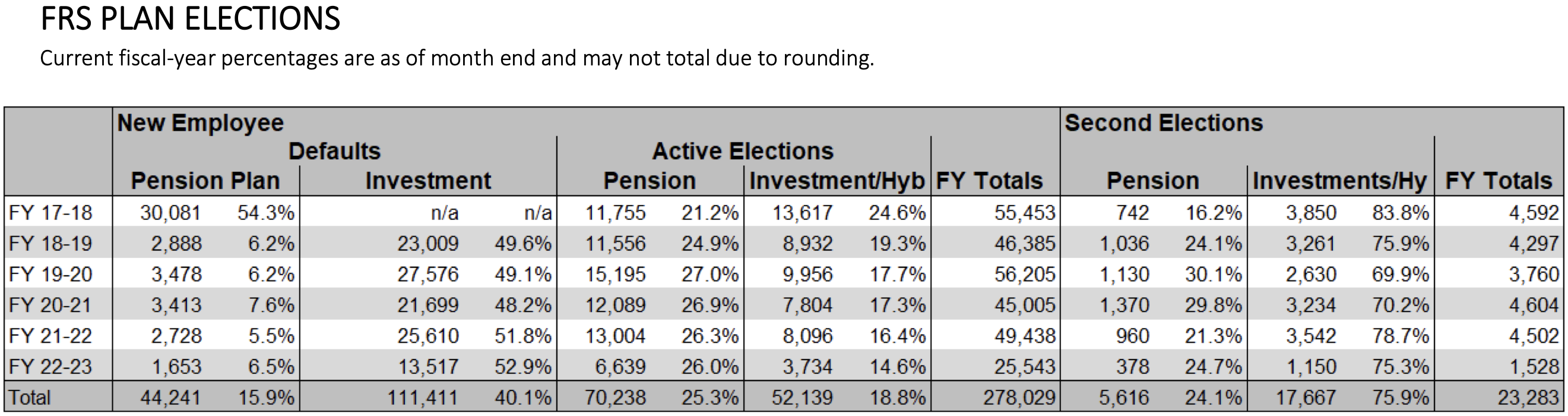

In the FRS Fiscal year of 2021-2022, 78.3% of 2nd Elections made by FRS members were comprised of pension members exiting the pension plan to opt for the smaller but much more rapidly growing Investment Plan. Why is that? There could be two reasons. The first, which we've written about before, is the potential to seek higher income in retirement from investment gains than the traditional pension plan, but there could also be a deeper reason. The overall health of the pension plan has fundamentally changed in the past two decades, and members are slowly becoming aware of this fact.

We meet many FRS members who say the only reason they choose the pension plan over the investment plan is because of the safety of the funds being invested in the pension fund. So here is a quick dive into what those numbers actually look like from the FRS directly in their annual report rather than spoken word.

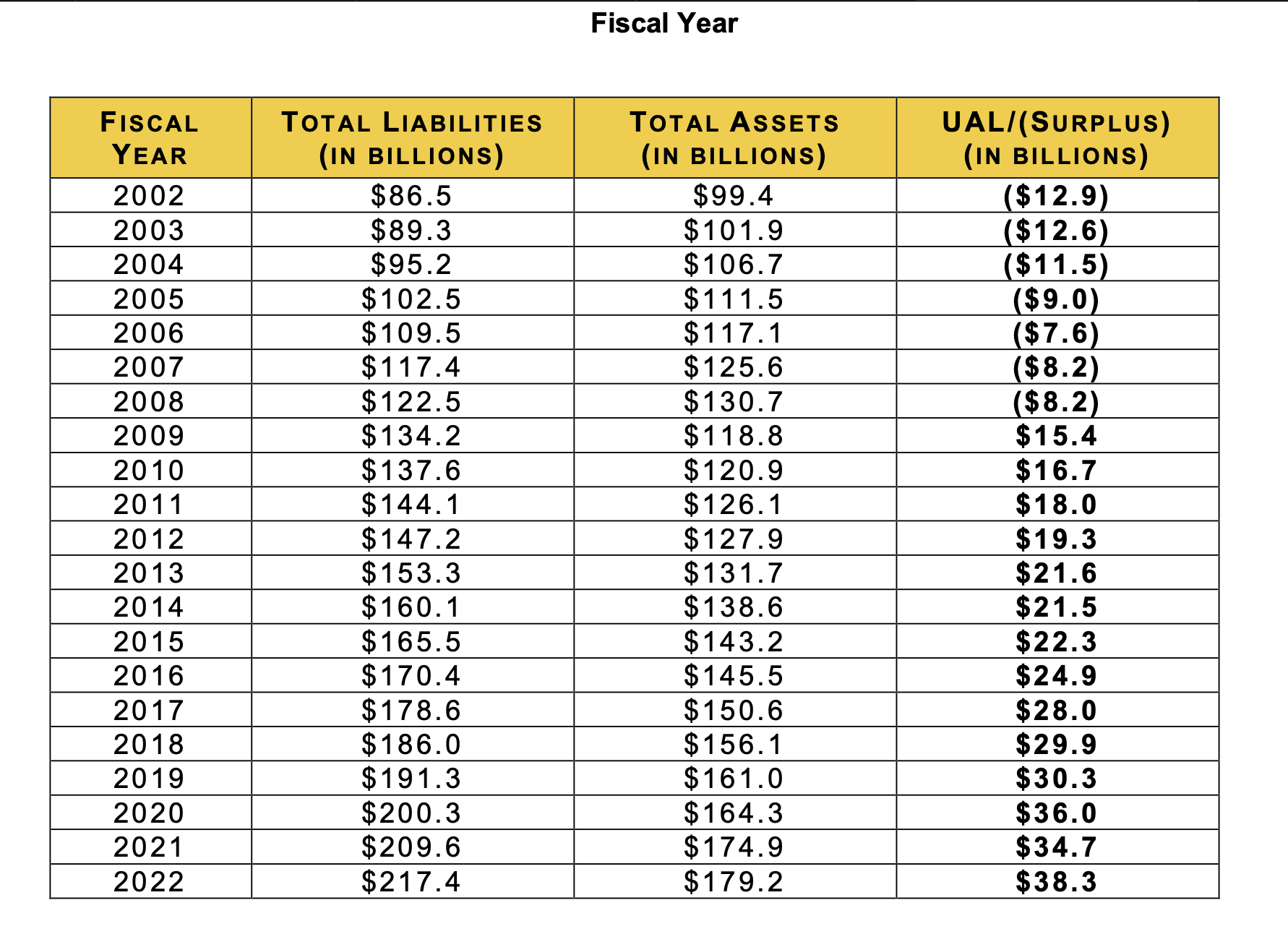

If we look back 20 years ago, in 2002 the FRS pension fund total assets were $99.4 billion, with only $86.5 billion in liabilities, meaning the plan was operating with a surplus of $12.9 billion. This appears to be a healthy funded ratio, but that surplus was shrinking every year until 2009 when the funded ratio turned over to operate with liabilities exceeding assets by $15.4 billion. Fast forward to 2022, and that deficit has increased to $38.3 Billion. This is illustrated below.

So how did this happen?

There are multiple factors that have contributed to this occurrence, but we will highlight the three most prominent.

1. The 2008 Great Recession caused a depreciation of assets within the FRS pension fund. An important fact many FRS members are unfamiliar with regarding the pension plan is that the assets in the pension fund are also invested. In many ways the investments are similar to fund options that are found in the investment plan. This carries an inherent amount of risk that with a resulting depreciation in fund assets in the 08-09 fiscal year. This can be seen in the previous graph when we look at plan assets in 2008 at $130.7 billion, and then decreasing $11.9 billion during the recession. This depreciation negatively impacted the ability for the pension funds to grow as liabilities also grew that year from $122.5 billion to $134.2. This means that the pension plan had $11.9 billion less to use to pay plan liabilities, and had $11.7 billion more to pay. Those liabilities have continued to increase since then, and plan assets have not been able to grow quickly enough to start finding a new equilibrium.

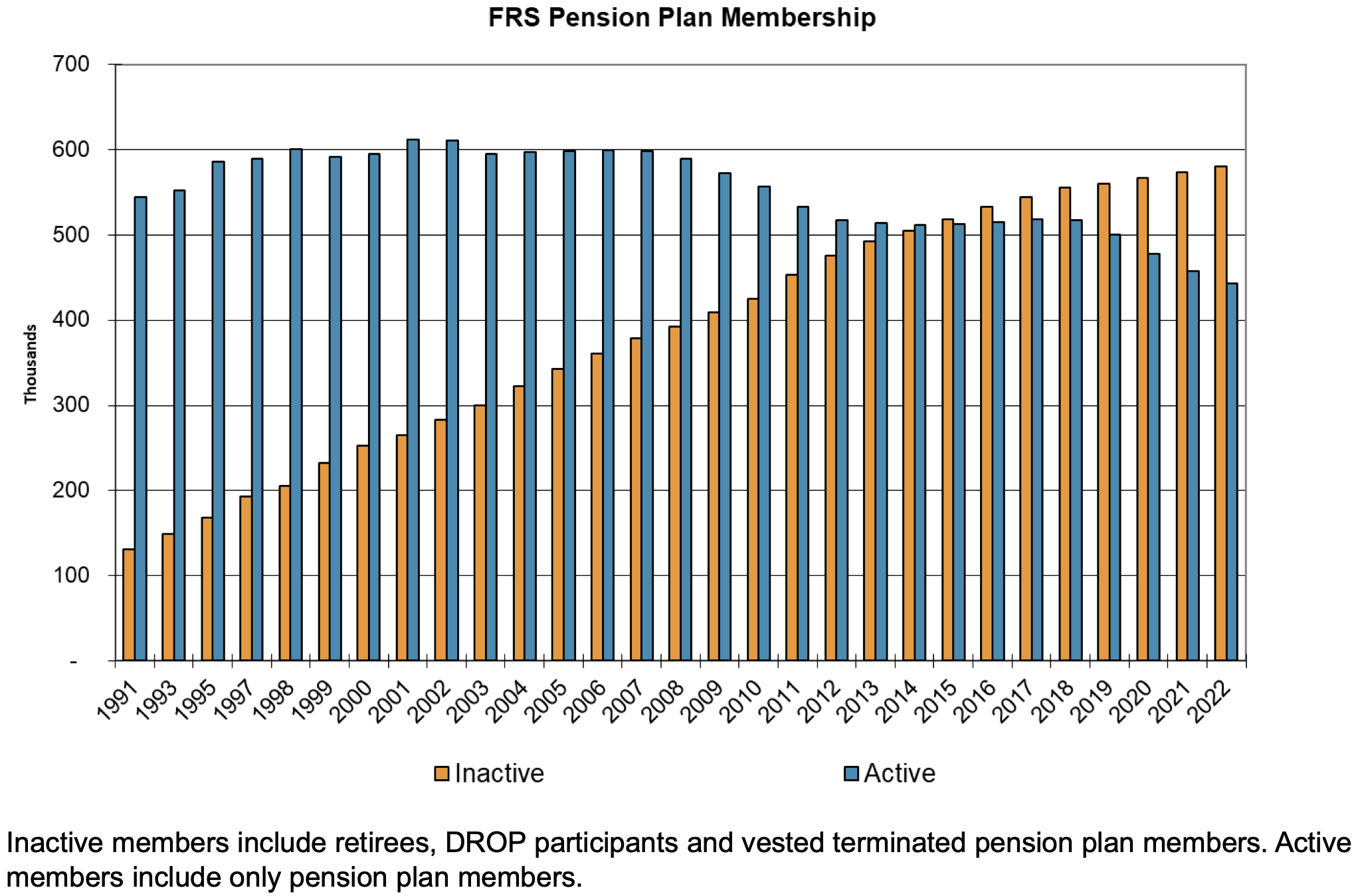

2. The 2nd factor is the increase in retirees over the past decade. The following graph from the FRS's annual report from the SBA details active members contributing to the FRS pension fund as well as retirees collecting a benefit. You can see from the graph that in the 2015-16 fiscal year, the number of members retired and drawing a benefit exceeded the number of members actively working and contributing to the plan. This puts more downward pressure on the pension fund's ability to pay liabilities as it widens the gap between dollars in vs. dollars out.

3. The 3rd contributor is that in 2018 the FRS changed the default retirement plan from the pension plan to the investment plan for new hires (excluding special risk). As a result, the number of new hires entering into the pension plan in the 2017-18 fiscal year dropped from over 30,000, to under 2,900 in the following year as seen in the graph below. This means that there are less contributions going into the plan to pay for the liabilities that continue to increase as more members retire. By looking at the previous graph you can see a visualization of this change impacting active pension memberships vs. inactive as a result of the change in 2018. The graph shows the number of active pension members has steadily decreased as a result of the <90% decrease in new members.

So what now?

As you've now seen, the funding of the pension plan has been on a consistently downward path with funding for the past 20 years, and many FRS members are not aware of these facts as they begin to plan their retirement. Though these facts alone may not be cause for permanent change in one's retirement plans, all facts such as these should be considered when developing a retirement plan. If you have questions about your FRS retirement plan or benefits, you can schedule a complimentary meeting using the link below and we will be happy to help. Choosing your FRS retirement plan benefits can be one of the largest financial decisions of your life. When it comes to retirement, math speaks louder than words.

Annual Report: https://employer.frs.fl.gov/forms/2021-22_ACFR.pdf

This hypothetical examples included within this post are for illustrative purposes only and do not constitute tax, legal or accounting advice. For advice regarding your personal situation, please consult an appropriately licensed professional.